Furious Friday

Busting the myth that our big 4 banks are “Too Big to Fail” (Part 1 of 2)

Welcome to Finance and Fury, the Furious Friday edition!

Today’s misunderstanding is about the “Too big to fail” myth.

I want to tell you a story. It’s probably a relatively unheard-of story… of our “Big 4” banks and their recent history.

The whole point of this is to answer: Are financial collapses created by too many regulations, or not enough?

The answer seems to be that more regulation is the only way to solve future financial crashes and any financial collapse has had some form of regulation come out of it as a result. But, the aim of this episode is to see if this has helped or hurt the economy and the banks overall

Warning: The banking system is pretty complicated, so there’s some points in this episode that might be pretty in depth. But that seems to be the whole point of the financial system: Make it so complicated not many people know what is going on. I have tried to make this as simple as possible so hopefully it isn’t a bore.

In this episode: What we will go through

- Banking sector: Vertical integration – One single company controls several others along the supply chain = profits come from different activities in different areas

- Look at history repeating itself – Comparing Australia to the US between 1999 and 2008

- What really lead to the GFC, and how we may be blindly following the same path

- The big 4 banks – market share of the economy – the effects on the Stock Exchange and the population

Timeline: How did we get where we are now?

- Banks listed: early 80s to 91 for CBA – No guarantee on deposits at that point

- APRA Australian Prudential Regulation Authority – Regulation for Banks – has only been around since 1998

- Before this: The riskier banks wanted to be, the higher the interest rate they would need to offer

- Under tighter regulations, risky banks had to comply to less risky standards

- Goodbye risk premium on interest

- Regulations continued as normal for a while, until financial crisis:

- We had a scare in 2008 – during the GFC banks stopped lending to one another for short term funding for their expenses

- Banks who can’t operate shut doors. Lehman Brothers for instance

- Bank runs – Great depression in the US 4,000 banks closed from 1929 to 1933

- US banks started doing ‘bailouts’ – In essence, printing money to buy Mortgage Backed Securities off the banks (we’ll come back to this)

- Fearing a bank run in Australia – October 2008, right at the peak of the GFC, the Australian government decided to guarantee bank deposits

- This is new-Australian Deposit Insurance – Guaranteed for the public (ironically by the public as well)

- History has shown Government can’t risk the market effects of wiping out people’s bank deposits – especially when voters money was on the line

- A guarantee helps to calm the public – if a policy says the money is secure it must be!

- The Financial Claims Scheme (FCS) was created – emergency measure to secure the banking system.

- Who is eligible: Authorised Deposit-taking Institutions (ADIs) – bank, building society or credit union. This means that this money is guaranteed if anything happens to the ADI.

- It applies to all ADIs incorporated in Australia, including Australian-owned banks, foreign subsidiary banks, building societies and credit unions.

- ADIs insured for up to $1m

- Feb 2012 – Dropped to $250,000

Sounds good right? Nice and safe!

- Safety has a dark side – It isn’t really safety for us, but the Banks!

- Removes incentives for depositors to review a bank before depositing – Onus is taken off us

- Some banks could offer higher returns, if riskier.

- But with this it is all the same – almost zero risk – removed risk premium on interest

- What behaviours it incentivises

- Increased risk

- Insurance creates moral hazard – Insurance to cover risky actions

- Maximise profits as the risks are covered for the most part

- It really provides safety to banks, and they can increase their risks – like giving a gambler a guarantee on his losses if he made a risky bet?

- Increased risk

- Increased incentives to maximise profits

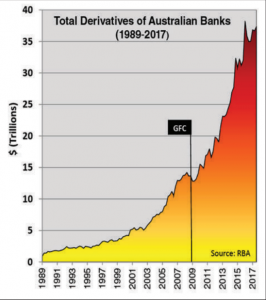

- But where from? Derivatives, asset backed securities and covered bonds – these can be risky

- Massive spike since 2011 of bank profits coming in the form of derivatives

- Derivatives: Complex financial bits of magic

- The options – Forward & Future Contracts, swaps, etc.

- Locking in rates now for the future

- Asset Backed Securities – Investment with an underlying asset –

- MBS – CBA: in one security – $2.65bn in mostly AAA rated

- Covered Bonds – Change in regulation in 2011 = AAA rated bonds issued

- Debt instruments covered by mortgages

- Sitting at over $80bn in value since 2011

- One difference is issuer covers bonds if they default, not on securities though

- The options – Forward & Future Contracts, swaps, etc.

What stops this all going wrong: APRA has to overregulate in response –

- Strong regulatory intervention through the (APRA).

- Australia has strong regulation but even the best regulation can be gamed.

- They have to be closely monitored by APRA – But banks are still incentivised to take on more risk

- Derivatives are held ‘off the books’ and very hard to regulate

- NAB and CBA stopped disclosing theirs, so who knows what their current levels are?!

Why does it matter? What happens to just 4 banks has an affect on everything!

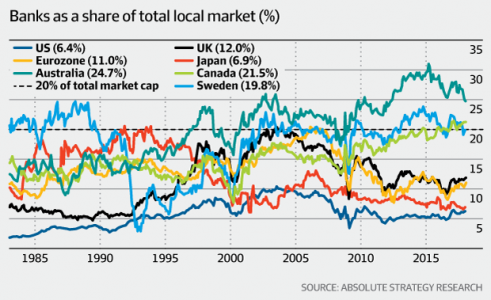

Where we sit today: The big 4 = 25% of the ASX

- The ASX is one of the most concentrated in the world

- Financials – 35% of our index, 25% is just the big 4 banks

- What is the fate of our market if the big 4 tank?

- We saw it in the GFC

- Declines in the banks of over 50% = Big drop in index and panic selling across the board

- If our banks rise, our market does, they fall, we all suffer, because the government will print money to stop the collapse (bailouts!)

- Double death! – Both Equity and Debt markets – Comes from regulation. Used to be just one at a time

Why are just 4 banks so big? The regulations lead to concentration at the top – Economies of scale to survive

The banks love (or loved – see the Banking Royal Commission) vertical integration! It was needed to survive in the regulatory world.

Current state of the banks

- 1991 – Commonwealth – Bankwest (2008), Aussie, Colonial First State

- 1982 – Westpac – RAMS, St George (2008), BankSA, Bank of Melbourne, BT

- Hastings (Infrastructure), Ascalon, Advance, Securitor, Magnitude

- 1982 – NAB – Ubank, MLC, Banks of New Zealand

- JBWere

- BOQ – Virgin Money, Investec Bank, Home Building society

- Bendigo bank – Adelaide bank, Delphi Bank, Rural bank

The party is over for most as they are selling other divisions: CFS for CBA

Hopefully the vertical integration can be looked at – A brief history of things:

- It was similar in the US: Has the guarantee $250,000USD, however something went wrong

- Glass-Steagall – Part of the 1933 Banking Act of the USA – Prohibited vertical integration

- Congress debated bills to repeal Glass–Steagall’s affiliation provisions (Sections 20 and 32). In 1999 Congress passed the Gramm–Leach–Bliley Act, also known as the Financial Services Modernization Act of 1999, to repeal them – But not the guarantee (almost the same place as our system since 2011)

- How much safety does the guarantee provide to the public? They had it in the US, but that arguably lead to the banks behaviours – Look at this in next Fridays episode

- How bailouts are funded through “Quantitative Easing” as it was called in the US, but it is printing money by any other name

- What allows for these bail outs, where the money comes from and the flow on effects of cash advancing your unlimited credit card, but at the government level it is ‘Quantitative Easing’

Thanks for listening! Next Friday we look at Part 2 of this question