Welcome to Finance and Fury. One major issue for shares in Australia and around the world – with the lock downs and companies bottom lines being affected – Dividend cuts on the rise

In this episode we will look at the ASX and the dividend cuts. We will also cover which sectors are being affected and the overall drops compared to previous crashes, along with if there is an opportunity out these in this.

What has happened?

- If you have been living under a rock – The response from governments to manage Covid led to significant changes in daily life – also has had significant impacts on economic growth globally and in Australia

- 2020 will likely be one of the worst years on record for global developed economies as the impacts of forced shutdowns halts economic output – created unprecedented levels of economic uncertainty

- Forecasts from the RBA show the Australian GDP to contract by 6% in 2020, and June 2020 unemployment to be 10% – numbers might not be as bad as initially thought – see what happens next month – but what has happened is that listed companies are taking action at the board level on their dividend policies

- Dividends – These are profits paid out – if you are a shareholder – you are an owner in the business – therefore the company makes a profit – you should be entitled to some of this – DPR at the board level decides how much

- Dividends have had a massive impact on returns for the ASX over any other market –

- Over the past decade, the total return for the S&P/ASX 200 was 7.1% pa – of which 6.1% (about 87% of that total return) was from dividends including FCs – 0.9% price, 1.6% FC and 4.5% dividend over past 10 years – Dividend payments in Australia totalled $80 billion last financial year

- Our market has been fairly reliant on dividends as part of a total return – so the cuts to these in the short term makes for a poor total return unless price gains pick up the slack this year –

What does that mean for company earnings and dividends?

- The change in economic conditions has had a severe impact on the outlook for earnings over the next year

- Many companies have abandoned earnings guidance due to the extreme uncertainty around when some level of normal will return to business conditions and confidence

- At the same time – Capital raisings have been frequent (and in relatively large size, as they were during the GFC) to keep companies capital in a safe position –

- Prices of shares have reacted strongly to this news – yield stocks (like the banks) have been some of the worst performers in the ASX 200 – if Divs are cut these goes your returns

- Since the middle of February, over 30% of companies in the ASX200 have deferred, cancelled, suspended, or revised dividends

- 13% deferred payment, 4% cancelled, 4% suspended, 4% no dividend, 1% revised

- The cuts to dividends have been a significant headwind for yield-focussed portfolios

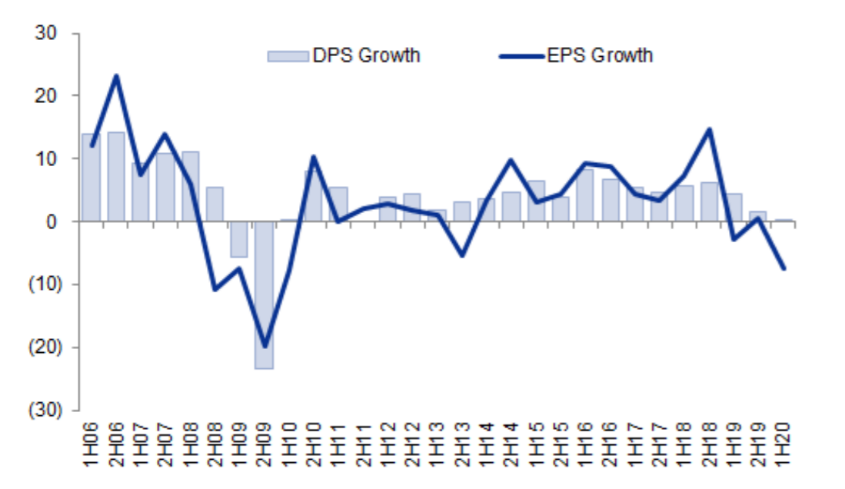

- DPS and EPS growth were already low before lock downs –

- EPS is the profits – DPS is how much of that is paid out – the market DPR was high – banks sitting at about 80% – so if profits drop by 20% – means no retained earnings – so drop DPS

- The ASX200 did have a high concentration in its income yield – Over 50% of dividends are paid by just eight companies – two-thirds of dividends paid by 18 companies – at the index level leaves market susceptible to the larger companies (banks) cutting dividends – like they currently are –

What sectors will be the most affected in the ASX200 and their weighting on dividends

- Low risk

- Supermarkets, telcos, pharma, tech, gold and iron ore

- 64 shares making up 30% of dividend weights

- Possible cuts in 2020 and 2021 – 5% and 0%

- Medium risk

- Financials, building/construction, discretionary health care

- 107 shares making up 30% of dividend weight

- Possible div cuts in 2020 and 2021 – 33% and 20%

- High risk

- Travel, entertainment, casinos, shopping centres, energy (oil)

- 27 shares making up 10% of div weights

- Possible div cuts in 2020 and 2021 – 100% and 33%

- The outlier – banks 7 shares making up 30% of weight – Possible div cuts in 2020 and 2021 – 60% and 50%

- In total – average of 40% to ASX200 in 2020 – then 24% in 2021

- The big 4 – Australian banks have historically been key features of any yield portfolio due to steady franked dividends

- Unsurprisingly -they have been amongst the worst hit through the COVID-19 market downturn, as economic activity slows and net interest margins shrink (as a result of lower interest rates); from the market high on Feb 21st to the bottom on Mar 23rd Australian banks fell an astonishing 44%, underperforming the ASX200 index by almost 10%

- Also – whilst the market has rallied off the bottom through April and into May, banks are down 37% from the February market high – no real really in the banks seen

- Three of the big four banks acted quickly announce their dividend decisions; ANZ suspended its interim dividend, NAB cut its interim dividend by 64% (to 30c) and announced a $3b capital raising, and WBC deferred its interim dividend decision without a set timeline for a decision – Westpac’s dividend suspension was the first such move by the bank in at least 37 years

- Still – the options for a lot of companies is to pay out all retained earnings and go bankrupt – so share values go to $0 or to hold the earnings and raise some capital if needed – so they can slowly recover over time and start paying dividends again

- At the moment though – the relative fall in price of banks mean they now trade on a forward dividend yield of 4.3% vs ASX200 at 3.6% – over the long term though – price and yields do change –

- Ex-CBA, the major banks are now trading on less than 1x book value, cheaper than the valuation in the depths of the GFC (CBA is now around its GFC trough book value multiple) – seems to show that the risks to the banks are well and truly factored into the price – along with investors jumping ship if they aren’t going to get Divs – which is the banks way of providing a return

- At the moment – banks are focusing on building up capital and retaining profits – means for now that the era of big bank dividends is on pause – for the short to medium-term – probably next 1-2 years – but given that the banks are forecasting bad loans rising from those who deferred loans cannot repay them in October – the reinstatement of dividends will be driven by how well the economy can emerge from its enforced hibernation

- One issue with capital raisings – will likely drop EPS and DPS going forward – NAB over past 10 years increased shareholdings by 30% – the $3b capital raising and $500m SPP will increase this by a further 7% of shares outstanding – so assuming total profits are the same – drop EPS by the same percentage

This won’t last forever – Long term – these is opportunity in markets that have traded down due to the dividend decisions – assuming that these companies survive and don’t have to take on massive debt.

- Even though we are now seeing similar dividend reactions as in the GFC for a lot of companies – the low-price entry opportunities offer investors access to potential future outperformance in stocks whose dividends are relatively untouched at the moment –

- Especially in the banks – the banks themselves and their success is linked with the economic outcomes – borrowing and confidence – so if the economy recovers and goes back to normal – so will the bank

- As we have seen – when the economy has a downturn, they will struggle a little bit

Summary –

- The price drops in markets initially – especially in yield stocks has been unlike anything seen in markets since the Great Depression – But at the same time there has also been an unprecedented response from governments and central banks via fiscal and monetary stimulus

- When the recovery begins is uncertain and dependent on numerous factors, but economies will recover and with it – Company earnings will recover as we move through the next year -with that dividends will eventually be reinstated – but still – Investing for yield has had a very difficult 2020

Yes – DPS and EPS will likely fall – comparing to GFC – and past events – dividends for companies that survive come back – so investing in companies that have the ability to weather the storm is important

- But shares are meant to be a long term investment – those who these policies most impact are those relying on dividend income to sustain themselves in retirement –

- Why having a cash buffer is very important – but longer term –

- The price of the market may slide further from here but if they do – good opportunity to lock in gains for the long term –

- The market is relative – buying now based on price is better than 4 months ago – not as good as 1 month ago – but may not be as good comparing to 6 months from now if the enthusiasm in the ASX runs out

- Still – rather than relying on the index – contrarian active approach can help to avoid these types of losses

Thank you for listening to today’s episode. If you want to get in contact you can do so here: http://financeandfury.com.au/contact/